Access Is Not Private Markets' Problem Anymore (but That's Not Enough)

The Click-to-Enter is there, not the Click-to-Exit...

Yesterday I rediscovered the fascinating story of late Jimmy Lee, formerly vice chairman of JPMorgan Chase & Co, but, above all, the man who invented the syndicated loan market and “made debt liquid”. Hat tip to Marc Andrew.

One of the sentences from Marc’s story resonated and stayed with me:

The "Wallet of Wall Street" didn't build infrastructure first. He proved liquidity was possible, and the infrastructure followed.

The liquidity he created “helped finance deals that remade entire industries and upended some of the mightiest companies in the land.”

Liquidity is the true transformational element of the private markets. Only when loans became more liquid, banks could transfer risks and keep financing new deals.

The way I thought about this is that the private markets have built infrastructure before finding its liquidity.

I am stretching the parallel a bit. But just a bit.

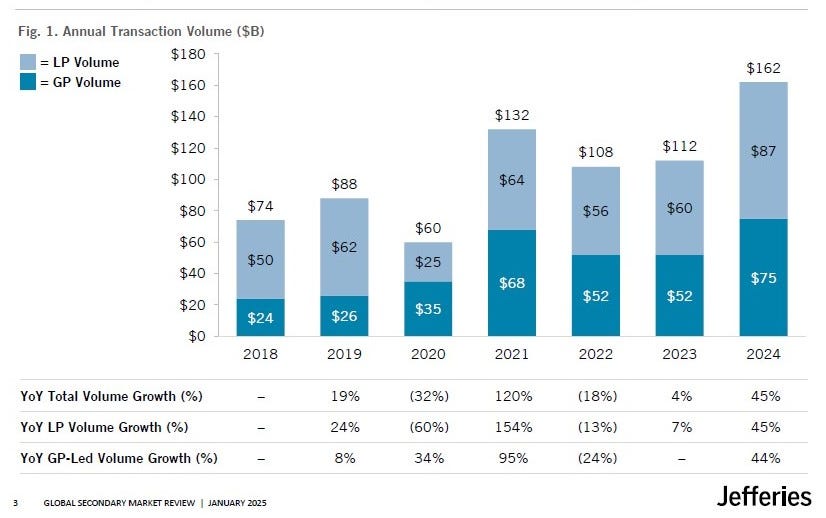

But the fact is that even the growing secondary volumes have been amplified by GP-leds that I would not consider “exit” liquidity. GP-leds, seen from a substance perspective, extend the duration and market risk of the investor who stays invested.

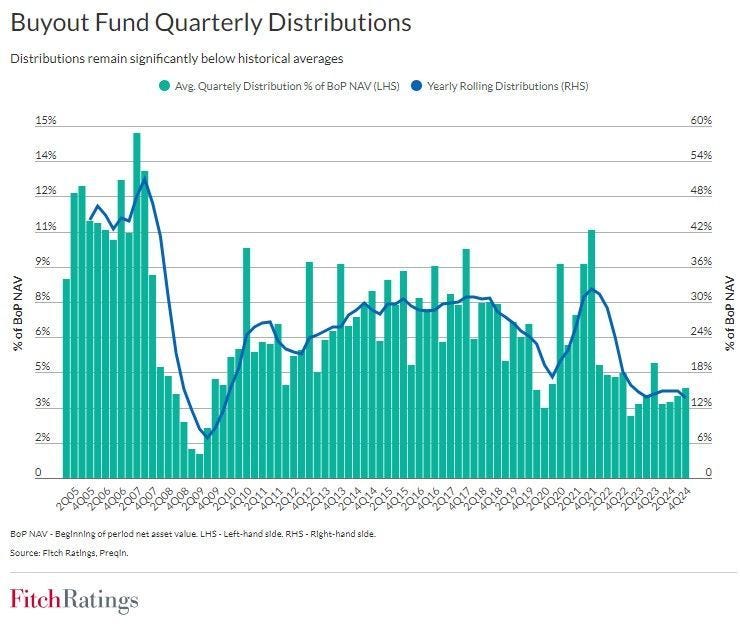

The intrinsinc liquidity of the system has been shrinking. DPIs have been worsening when the secular trend of downward interest rates has ended.

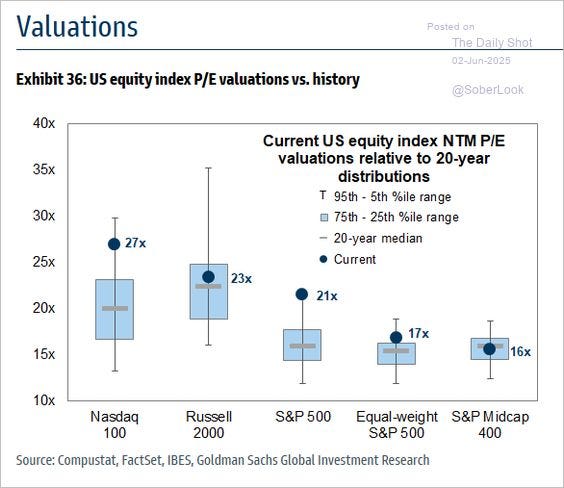

High valuations in the listed markets are keeping multiples up in the private markets too but have not restarted the IPO liquidity / exits engine.

Infrastructure for access is ready, even for full democratization. Cash can enter the private markets, in a variety of forms and from almost all channels now.

Players, platforms, contracts, even regulators’ consent, are there. Evergreen vehicles, interval funds, Eltifs 2.0 are broadening the reach of private market offerings, traditionally limited by institutional closed-end structures.

Instead, the required two-way liquidity that would extract the full potential of the industry is not there yet.

Two-way means that given the uncertainty of the exits at portfolio company level (cash-flow are a function of duration and market risk), secondary trading decisions are a last resource option. Investors activate a sale process just if they need cash and not because a different allocation has a better marginal return.

I am talking about financially rational pricing, which requires the possibility to determine relative values between alternative choices, in real time and not as an ex-post exercise.

Only by changing the valuation paradigm to the time-weighted framework of traditional asset classes, technology that produces valuable information can be developed.

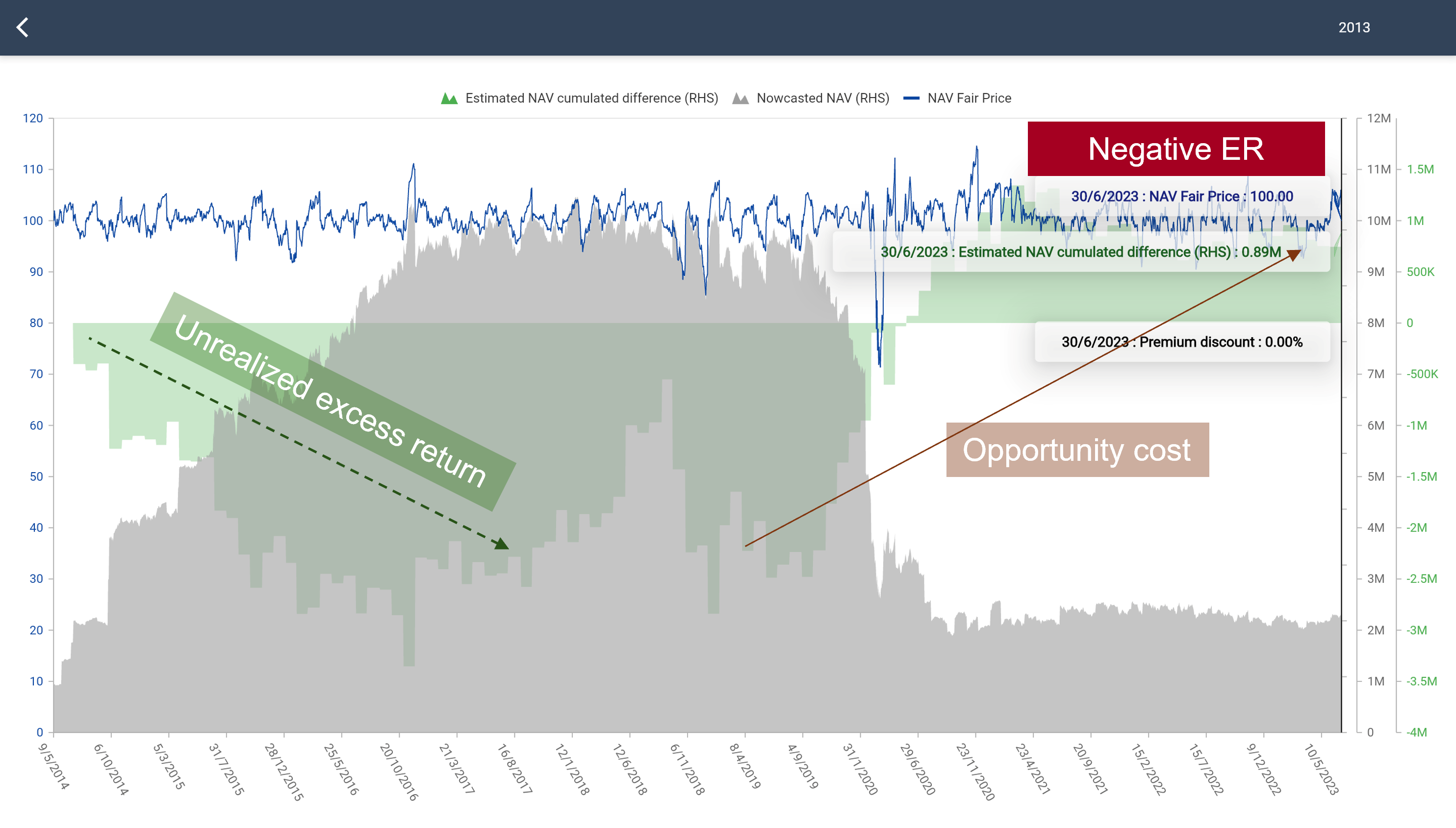

As an example of such technology, a coherently built model provides NAV nowcasted estimates (in grey) and “cumulated error” information (in green) in real time .

Error in negative territory shows potential model underestimation of NAV (either potential or realized Excess Return (ER). Model underestimation may indicate an opportune moment for selling on the secondary market to capture excess return.

Please note thought that excess return is true if it materialised during the progressive liquidation of the underlying portfolio at higher values than those provided by the model.

The chart above shows instead that excess return, in the anonymized case of a 2013 secondary fund, did not materialize.

On the contrary, it looks that patience did not pay out.

Patience is never a mantra with investments.

You can also follow my updates on LinkedIn for more private market insights.